Reconnecting Syria: People, Trade and Recovery Through the Lens of Border Data, 2024-2026

Following the collapse of the Assad regime in December 2024, Syria’s border crossings have undergone a dramatic institutional overhaul and a surge in commercial activity — tracked here across land, sea, and air entry points through early 2026.

The fall of the Assad regime in December 2024 triggered a rapid, if turbulent, reopening of Syria’s commercial and trade corridors. Within days of the transition, new governing bodies were stood up to manage land, sea, and air border points — and the data collected since then tells a story of accelerating trade recovery punctuated by protectionist disruptions, major port concession deals, and a civil aviation sector reviving from near-zero.

This briefing aggregates publicly available datasets and official statements from the Syrian General Authority for Land and Sea Border Crossings (subsequently restructured as the General Authority for Border Crossings and Customs), Syrian General Authority of Civil Aviation and Air Transport (GACA), the United Nations Logistics Cluster, and bilateral trade data from Jordan, Türkiye, and Lebanon. It covers the period from December 2024 through February 2026, spanning Syria’s first full calendar year under transitional governance.

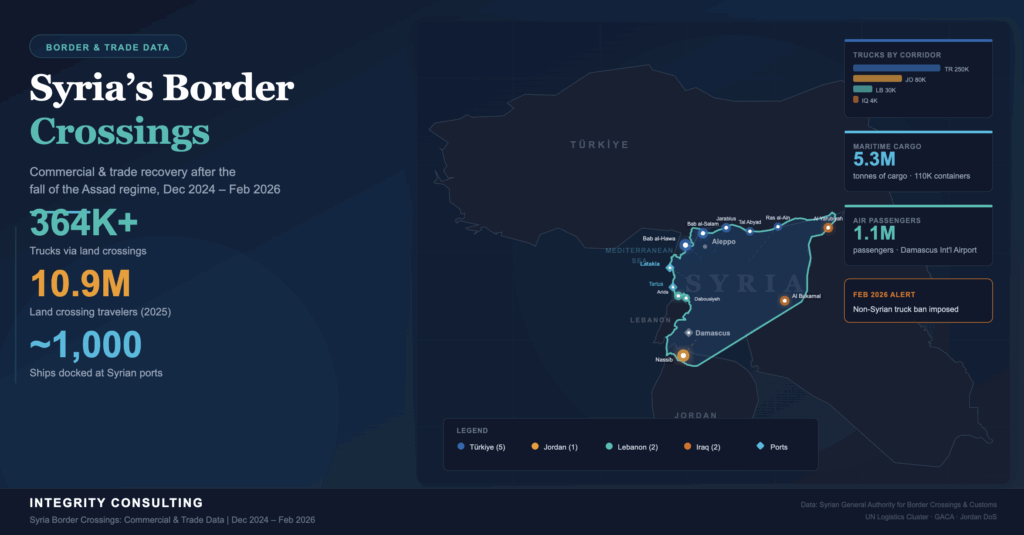

The data reveal a country reconnecting with global trade at speed: over 364,000 trucks moved goods across land crossings in the first nine months alone, Syrian ports welcomed nearly 1,000 ships, and international flights resumed at Damascus International Airport in January 2025 after years of conflict-era restrictions. Yet persistent infrastructure deficits, aging transport fleets, and the February 2026 ban on foreign trucks have introduced friction that threatens the momentum of the recovery.

UN Logistics Cluster · GACA · Jordan Department of Statistics · Türkiye Ministry of Trade

Jan–Dec 2025 · Official General Authority data

Click a gate marker for details

Land crossings, Dec 2024 – Aug 2025

Ring = UN Logistics Cluster gate · Size = volume

110,000 containers (Dec 2024–Nov 2025)

Click anchor marker for port details

Institutional Reform: The New Border Authority

On 31 December 2024, just weeks after Assad’s fall, the Syrian Prime Ministry announced the creation of the General Authority for Land and Sea Border Crossings — a new body attached to the Council of Ministers with administrative and financial independence. The move dissolved the former customs police structure, with the new Director General issuing a formal decision on 18 December 2024 to reconstitute it in a manner that “serves the public interest.” By 25 December, the General Customs Directorate had already dismissed and replaced border crossing directors at multiple land and sea points.

The institutional architecture was restructured again in November 2025. Presidential Decree No. 244 established the General Authority for Border Crossings and Customs, reporting directly to the Presidency of the Republic rather than the Council of Ministers. The decree consolidated oversight of land and maritime crossings, free zones, customs, port management, and maritime transport under a single body — an arrangement commentators described as a centralisation of Syria’s financial and frontier gateways. Qutaiba Ahmed Badawi, who previously oversaw commercial operations for Hay’at Tahrir al-Sham including management of the Bab al-Hawa crossing, was appointed head of the new authority with ministerial rank.

The new authority’s mandate extends beyond day-to-day operations: it is tasked with developing unified electronic interconnection between crossings, ports, and free zones; adopting international digital standards; and representing Syria in relevant regional and international organisations. In practice, the first 14 months of the transitional period have been marked by a tension between the speed of commercial recovery and the institutional capacity to manage it.

Land Border Crossings

Syria’s land border network connects the country with Türkiye to the north, Jordan to the south, Lebanon to the west, and Iraq to the east. The Nassib-Jaber crossing (Syrian-Jordanian border) and the Bab al-Hawa and Bab al-Salam crossings (Syrian-Turkish border) are historically the highest-volume commercial points. The collapse of the Assad regime in December 2024 allowed the government to reassert control across most of these crossings for the first time since the civil war fragmented Syrian territory.

Between December 2024 and the end of August 2025 — a nine-month window — Syrian border crossings registered more than 364,000 commercial trucks carrying over 8.7 million tons of goods. This represents a significant rebound from the near-total disruption of the conflict years, when land trade was channelled through a patchwork of faction-controlled crossing points with inconsistent procedures and revenue capture.

Dec 2024 – Feb 2026

(Dec 2024–Aug 2025)

via land crossings

full year 2025 (official)

Syrian truck fleet

-

18 Dec 2024Nassib-Jaber reopened — First Jordanian trucks enter Syria directly via the main southern crossing.Operational

-

31 Dec 2024New border authority created — General Authority for Land and Sea Border Crossings established under Council of Ministers.Institutional

-

Jun 2025Syria-Türkiye road transport MoU signed — Reactivates 2004 bilateral agreement; covers trucks, transit, Ro-Ro, driver visas & technical standards.Diplomatic

-

14 Jul 2025All Türkiye crossings go 24/7 — Round-the-clock operations activated to manage mass return of 3.5M Syrian refugees from Türkiye.Expanded

-

Aug 2025Turkish-entry simplified — Syrians may cross from Türkiye without prior permission; advance authorisation requirement removed.Expanded

-

Sep 20259-month cumulative data published — 364,000+ trucks, 8.7M tonnes, 6.8M travelers confirmed by General Authority public relations office.Data

-

Nov 2025First Türkiye-Gulf transit convoy — First transit convoy crossing Syrian territory toward Gulf countries in years; enters via Cilvegozu/Bab al-Hawa.Milestone

-

Jan 20262025 annual data published — General Authority records 10,854,511 land-crossing travelers for full year 2025: Lebanon corridor 49.3%, Jordan 27.6%, Türkiye 22.1%, Iraq 0.8%. Voluntary returnees totalled 994,935. Damascus Airport: 146,219 passengers in November and 165,714 in December 2025.Data

-

6 Feb 2026Non-Syrian truck ban imposed — All foreign trucks prohibited from entering Syria; back-to-back transfer only. Costs doubled from Jordan; 50–70% rise from Türkiye/Lebanon.Disruption

A notable development in July 2025 was the decision by the General Authority to open all Syrian border crossings with Türkiye on a 24-hour, seven-day-a-week basis, effective 14 July. The move was designed to reduce congestion and facilitate the large-scale return of Syrian nationals from Türkiye, where an estimated 3.5 million Syrians had sought refuge during the conflict. In August 2025, the Authority further announced that Syrian expatriates could cross from Türkiye without prior permission, simplifying a procedure that had required advance authorisation since July 9.

Also in June 2025, Syria and Türkiye signed a memorandum of understanding to reactivate cooperation in international road transport — resuming an agreement originally inked in May 2004. The MoU covers truck crossings, transit movement, Ro-Ro facilities, visa facilitation for professional drivers, and harmonisation of legislative and technical standards. By November 2025, Syria’s Ministry of Transport announced the passage of the first transit convoy crossing Syrian territory toward Gulf countries from Türkiye — the first such convoy in years — entering via the Cilvegozu/Bab al-Hawa border crossing.

Sea Border Crossings & Ports

Syria’s maritime trade flows primarily through two Mediterranean ports: Latakia, the country’s largest seaport and principal container hub, located approximately 40 kilometres from the Turkish border; and Tartus, Syria’s second port, historically specialised in bulk cargo including petroleum and agricultural commodities. Both ports suffered operational degradation during the conflict years and were previously entangled in Russian and Iranian lease arrangements.

From December 2024 through August 2025, Syrian ports registered the docking of nearly 1,000 ships with a combined cargo volume exceeding 5.3 million tons — a figure the transitional government cited as evidence of recovering maritime trade. Over the longer period from December 2024 through November 2025, the ports of Latakia and Tartus together handled 110,000 containers, coinciding with the acceleration of sanction relief and new port concession agreements.

Port of Latakia — CMA CGM Concession

In May 2025, Syria entered a 30-year agreement with French shipping giant CMA CGM to operate Latakia port. The deal hands management of Syria’s primary container hub to a global logistics operator, replacing an era of state management during which the port’s throughput declined sharply from a pre-war peak of 8 million tons (2008).

Port of Tartus — DP World Concession

A $800 million, 30-year memorandum of understanding was signed between Syria’s General Authority and Dubai-based DP World in July 2025. DP World formally began operations at Tartus in November 2025, committing to upgrade infrastructure, expand container handling and storage capacity, and develop industrial free zones and dry ports at strategic locations across Syria.

First Phosphate Export & China Trade

In April 2025, the first ship loaded with 10,000 tonnes of Syrian phosphate departed from Tartus — a key indicator of resuming commodity export capacity. By October 2025, Tartus had received its first direct shipment from China since the fall of the regime, signalling the restoration of a critical trans-Mediterranean trade corridor.

Russian Naval Presence Under Renegotiation

Russia previously held a 49-year lease on Tartus port for its only Mediterranean naval base, signed in 2019. Following Assad’s fall, the Syrian transitional government moved to unwind these arrangements: by October 2025, reports indicated that President al-Sharaa had discussed terms with Moscow, and the subsequent DP World concession effectively displaced Russian civilian port operations.

Grain & Food Security Imports

In September 2025, two ships carrying Ukrainian wheat arrived at the ports of Latakia and Tartus under bilateral contracts — the first such shipments since the war disrupted Syria’s grain import channels. The arrivals marked a restoration of a critical food supply corridor for a country estimated to have 12 million food-insecure people.

Free Zone Investment Opportunities

More than 500 investment opportunities were launched in Syrian free zones between December 2024 and August 2025. Key zones include Latakia Port Free Zone, Tartus Port Free Zone, Damascus International Airport Free Zone, and the Aleppo and Adra Free Zones. These zones offer tax and duty exemptions and freedom to transfer capital and profits.

Air Border Crossings

Syria’s civil aviation sector was among the most visibly affected by the transition, and its recovery has been among the most quantifiable. Damascus International Airport (IATA: DAM) — the country’s largest airport, capable of handling virtually all aircraft types including the Airbus A380 and Boeing 747-8 — resumed commercial operations on 18 December 2024 with the first domestic flight to Aleppo. International flights resumed formally on 7 January 2025, the first since the regime’s fall.

Aleppo International Airport reopened in March 2025 following a comprehensive rehabilitation programme that included upgrades to the parallel runway with navigational lighting, restoration of the security perimeter, and enhancement of air traffic control communication systems. Passenger halls, immigration, and customs facilities were also refurbished. Seven airlines were operating at Aleppo by October 2025, when the airport handled 33,000 travelers on 370 flights in a single month.

Damascus International Airport & Aleppo International Airport

The Syrian General Authority of Civil Aviation and Air Transport (GACA) reported in August 2025 that 5,326 aircraft were recorded in transit over Syrian airspace that month, representing a 37% increase over July. By that date, more than 14 Arab and international airlines had resumed scheduled flights to Damascus and Aleppo — a nearly fivefold increase in air traffic compared to pre-transition levels. An air services agreement signed with the Sultanate of Oman in 2025 contributed to the expansion, with ongoing discussions targeting additional bilateral aviation agreements.

Air cargo data for Damascus International Airport showed 103 tonnes of outbound cargo and 23 tonnes of inbound cargo in October 2025, according to GACA. Damascus has two parallel runways (3,600 metres each), fully renovated in the 2010s. A landmark $4 billion agreement for the construction of a third passenger terminal was signed with Qatar’s UCC Holding in August 2025; the facility, inspired in geometric form by the Damascus sword, is intended to raise total airport capacity to 31 million passengers per year once complete. Rehabilitation of Deir ez-Zor Airport is expected to begin in 2026, further extending domestic air connectivity.

Trade Flows by Partner Country

The lifting of international sanctions — the EU in May 2025 and the US (via executive order) in June 2025 — unlocked bilateral trade growth that had been constrained since 2011. Mirror trade statistics from Syria’s partners provide the clearest available picture of the volume and direction of flows, given the acknowledged limitations in Syria’s own statistical capacity.

Year-on-year growth rates and absolute values where available

Türkiye is Syria’s dominant trade partner, with exports to Syria reaching $2.5 billion in 2025 — a 70% increase over the prior year and reflecting Türkiye’s role as the principal regional backer of President Ahmad al-Sharaa’s government. Syrian imports from Türkiye rose roughly 60% compared to 2024. However, Syria’s exports to Türkiye declined by approximately half over the same period — a dynamic generating frustration among Syrian industrialists who warn of a growing trade deficit.

Jordan’s bilateral trade with Syria almost doubled to $432 million in the first 11 months of 2025 compared to the same period in 2024, with Jordanian exports accounting for 66% of the volume — a 351% increase year-on-year, according to Jordan’s Department of Statistics. The volume of lorry traffic at the Jaber-Nassib crossing — the only land crossing between the two countries — far exceeded pre-transition levels: 150 lorries per day carrying goods from Gulf countries alone were transiting via Jordan’s Aqaba port into Syria by early 2026.

Syrian crude oil exports also resumed through maritime channels: in September 2025, Syria exported 600,000 barrels of heavy crude oil from Tartus, marking the first such shipment since the regime’s fall. Syria’s total exports for H1 2025 reached $580 million, a 39% rise over the same period the previous year, driven largely by agricultural commodities, phosphate, and early-stage oil resumption.

What Syria Exports: Products & Destinations

Syria’s export profile has undergone a fundamental structural shift since the onset of the civil war in 2011. Crude oil, which once accounted for 67% of total Syrian exports and peaked at around $12 billion in 2010, has been almost entirely displaced as the dominant export commodity. In its place, agricultural and food-based exports now form the backbone of Syria’s outward trade — led above all by olive oil, cotton, spices, nuts, and phosphates. In 2024, Syria’s total export value was approximately $820 million to $1.25 billion, representing an enormous decline from the pre-war level but a gradual recovery from the nadir of $554 million recorded in 2018. For H1 2025, total exports reached $580 million — up 39% on the same period of 2024 — with resumption of oil exports from Tartus in September 2025 expected to drive a further step-change.

Top Export Products (2024 — Estimated Values)

Estimated values: total export base ~$820M–$1.25B

Olive oil is Syria’s single most valuable export and a product of growing international commercial significance. In 2023, Syria exported $256.75 million in olive oil; by 2024, this figure rose to an estimated $303 million — an 18% increase year-on-year. Syria’s olive-growing regions, concentrated in the coastal mountains and the Idlib countryside, were among the areas that experienced the least agricultural disruption during the conflict. The lifting of EU and US sanctions has significantly expanded market access: EU member states — particularly Italy, Germany, France, the Netherlands, and Spain — are now the primary destination for Syrian olive oil, with the European bloc collectively absorbing a substantial share of the agricultural export portfolio.

Cotton has historically been Syria’s most reliable agricultural export crop, grown primarily in the Euphrates and Khabur river valleys. In 2024, raw cotton exports increased 5.6% year-on-year to approximately $52 million. The sector has significant recovery potential: pre-war, Syria’s vertically integrated cotton industry (from field to finished textile) was a cornerstone of the Aleppo and Damascus manufacturing base. Phosphate is the major mineral export, with Syria holding an estimated 1.7 billion tonnes of reserves near Palmyra. The first phosphate shipment since the transition — 10,000 tonnes departing Tartus in April 2025 — marked the re-entry of this commodity into global trade flows. Crude oil exports resumed through maritime channels in September 2025 with 600,000 barrels of heavy crude shipped from Tartus — the first oil export in 14 years following the removal of Western sanctions.

Iraq — Largest Single Export Market (20.2%)

Iraq absorbs roughly a fifth of Syria’s exports — an estimated $166M in 2024 — primarily agricultural products including fresh produce, processed foods, spices, and cotton goods. The Syrian-Iraqi land corridor via the Abu Kamal/Al-Qa’im crossing is the primary conduit, though volumes remain well below pre-war levels when the two countries were linked by a major commercial highway.

Italy & Germany — European Olive Oil Buyers (13.4% & 13%)

Italy and Germany together account for over 26% of Syrian exports — an estimated $213M combined in 2024 — driven overwhelmingly by olive oil imports. Both are major processors and re-exporters of Mediterranean olive oil, and Syrian product is prized for its quality. The lifting of EU sanctions in May 2025 significantly simplified the compliance burden for European buyers re-engaging with Syrian suppliers.

Türkiye — 5.5% of Exports ($45M) and Declining

Türkiye received approximately $45M of Syrian goods in 2024 (5.5% of Syria's total exports), but Syrian exports to Türkiye declined by roughly half in 2025 despite Türkiye being Syria’s biggest import partner. This asymmetry is a growing political tension: Syrian industrialists warn the trade deficit with Türkiye threatens local manufacturing, particularly in food processing, detergents, and consumer goods sectors.

Saudi Arabia, France & Jordan — Mid-Tier Markets

Saudi Arabia (4.8%), France (4.3%), and Jordan (3.6%) complete the top 10 Syrian export destinations. Lebanon historically absorbed significant Syrian exports — petroleum products, phosphates, cotton, barley, lentils, and dried fruit — though its 3.8% share reflects a fraction of the bilateral flows that characterized the pre-war relationship when Syria was Lebanon’s principal land trade corridor to the Arab world.

US, Netherlands & Egypt — Emerging Re-Entry Markets

The United States (3.5%), Netherlands (3.5%), and Egypt (3.4%) round out the top 12. US re-engagement accelerated from mid-2025 following the revocation of comprehensive sanctions effective July 1, 2025. The US market’s significance is expected to grow substantially from 2026 onward as American companies rebuild supply chain relationships with Syrian agricultural exporters, particularly in spices, olive oil, and specialty nuts.

Fastest-Growing Export: Live Animals (+178.8% in 2024)

Live animal exports were the fastest-growing Syrian export category in 2024, rising 178.8% year-on-year as livestock movement to Gulf and Arab markets resumed along reopened land corridors. Cotton also grew 5.6%. The steepest decliner was fresh vegetables (−71.9%), reflecting continued irrigation infrastructure damage, displacement of agricultural labour, and disrupted cold-chain logistics.

What Syria Imports: Products & Origins

Syria faces a deep structural import dependency that has intensified through the conflict years. Total imports in 2023 were approximately $3.64 billion, yielding a trade deficit of $2.93 billion. With sanctions lifted in 2025 and demand for reconstruction materials, food, fuel, and consumer goods surging, the total import volume for 2025 is estimated to have increased dramatically — far exceeding the 2024 figure of approximately $6.4 billion. Growth rates from individual partner countries confirm the scale of the surge: imports from Jordan rose 351%, from Saudi Arabia 223%, from Türkiye 60%, and from Lebanon 83%, all in 2025 compared to 2024.

Top Import Categories (2025 — Leading Products)

Year-on-year % change in imports into Syria by country of origin

Machinery & Industrial Equipment

The largest import category by value, and the fastest-growing in 2025. Turkish exports of machinery and industrial equipment to Syria surged 244% in January 2025 alone, reflecting acute demand for production inputs across manufacturing, construction, and agriculture. This category covers industrial machines, spare parts, construction equipment, cranes, generators, electrical appliances, and agricultural machinery. Suppliers include Türkiye (dominant), China, and increasingly EU member states following sanction removal. The World Bank estimates reconstruction costs at over $216 billion, virtually guaranteeing sustained heavy machinery import demand for years to come.

Fuel & Refined Petroleum Products

Despite Syria having domestic oil reserves (~2.5 billion barrels estimated), the destruction of refinery infrastructure during the civil war created severe dependence on imported refined petroleum products. Key imports include crude oil for refining, diesel, petrol, and natural gas. Principal suppliers shifted from Iran and Russia (which supplied heavily under the Assad regime) toward Türkiye (which began channelling Azerbaijani natural gas via the Kilis–Aleppo pipeline from August 2025) and Gulf states. The 2023 top import product in this category was refined petroleum products at approximately $95 million. Türkiye committed to supplying 900 MW of electricity by 2026 under bilateral energy agreements.

Wheat, Flour & Grain

Syria shifted from a net wheat exporter to a net importer — a structural change underscoring the depth of agricultural collapse during the conflict. Wheat flour was Syria’s single largest documented import product in 2023 at approximately $138.73 million. Principal suppliers include Ukraine (two ships carrying Ukrainian wheat arrived at Latakia and Tartus in September 2025 under bilateral contracts), Russia, and Türkiye. The wheat import bill is expected to remain high through 2026 as domestic production recovers only gradually from drought, displacement of agricultural workers, and landmine contamination of farmland.

Edible Oils (Sunflower, Cottonseed & Soybean)

Sunflower and cottonseed oil was Syria’s second-largest documented import product in 2023 at approximately $113.12 million. With domestic oilseed crushing capacity dramatically reduced, Syria depends on Ukraine, Türkiye, and Egypt for these essential foodstuffs. The category also includes soybean oil, used both for household consumption and as an industrial input in food processing. Demand has been compounded by the humanitarian situation: over 12 million Syrians remain food insecure, creating sustained pressure on edible oil import volumes.

Construction Materials (Cement, Glass, Ceramics & Metals)

Reconstruction demand is driving a surge in imports of cement, glass, ceramics, steel, and metals. Turkish exports of cement, glass, and ceramics to Syria rose 92% year-on-year in early 2025, while metal exports grew by 73%. These figures reflect the combination of reconstruction activity in liberated areas, urban rebuilding programmes, and private sector housing repair. Türkiye and China are the primary suppliers of construction materials, with Gulf-funded reconstruction programmes channelling procurement through Turkish and Qatari contractors. Iron and steel scrap — Syria also exports approximately 1.9% of its own trade in this category — is both imported and processed domestically.

Food, Consumer Goods & Agricultural Products

Turkish consumer goods — ranging from basic food staples (meat, canned goods, dairy), clothing, glassware, and household appliances to fruits and vegetables (which grew over 300% in Turkish exports to Syria in 2025) — now flood Syrian markets. Turkish goods are estimated to be priced 30–40% below equivalent local products, posing a structural challenge to Syrian domestic producers. Jordan exports food, cleaning products, pharmaceuticals, and processed consumer goods. Lebanon traditionally supplied agricultural produce, beverages, and chemicals. Saudi Arabia supplies consumer goods, petrochemicals, and food products; Saudi imports into Syria surged 223% in 2025. Egypt ($304 million in 2023) supplies food products, textiles, and basic commodities.

Pharmaceuticals & Medical Supplies

Pharmaceutical imports are a critical but data-scarce category. Syria’s domestic pharmaceutical industry — once one of the most developed in the Arab world, with production facilities concentrated in Damascus and Aleppo — was severely damaged during the conflict. Import suppliers include Türkiye, India, China, and EU member states. Human rights organisations flagged pharmaceutical and medical equipment imports as among the most urgently needed categories constrained by sanctions, and the removal of US and EU restrictions from mid-2025 onward has opened supply channels previously blocked under secondary sanctions provisions. The US Commerce Department specifically cited pharmaceuticals, medical devices, and telecommunications equipment in its September 2025 rule easing dual-use export licensing to Syria.

Vehicles & Transport Equipment

Motor vehicles, vehicle parts, and accessories form a significant import category, driven by the complete depletion of the civilian vehicle fleet during the conflict, reconstruction logistics demand, and the absence of any domestic vehicle manufacturing. Suppliers include Türkiye, China, South Korea, Germany, and Italy. The ageing Syrian commercial truck fleet — average age estimated at 30–40 years and widely criticised for posing safety and cargo risks at border crossings — is a systemic constraint that the February 2026 truck ban has made acutely visible. Fleet renewal is an implicit precondition for the protectionist policy to function as intended.

February 2026: The Non-Syrian Truck Ban

On 6 February 2026, Syria’s General Authority for Border Crossings and Customs issued a decree prohibiting non-Syrian trucks from entering Syrian territory through land border crossings. Under the new rules, goods must be transferred between foreign and Syrian trucks at the customs yard (“al-Tabbun”) at each crossing — a so-called back-to-back or transshipment arrangement. Transit trucks crossing Syrian territory toward third countries were exempted, provided customs police escort them between entry and exit points.

The Syrian government framed the measure as an economic necessity: Syrian truck drivers, who had been largely without work since 2011 when the conflict grounded the national transport fleet, had protested and in some cases attacked foreign drivers. The decree aimed to restore freight revenues to domestic transporters. Muhammad Kishour, president of the International Union of Goods Transport Companies in Syria, described it as a long-overdue corrective, noting that Syrian trucks had been excluded from return loads in Lebanon and Jordan for years.

The practical impact has been severe. Most Syrian transport vehicles are reported to be 30 to 40 years old, with many drivers working independently of registered companies. Border crossing infrastructure — the yards, loading equipment, and logistics capacity needed to support high-volume back-to-back transfers — is inadequate at most crossings. Perishable goods have spoiled during delays. Consumer prices in Syrian markets have risen, with particular concern raised ahead of Ramadan 2026 and its associated spike in demand. Lebanon, whose truck drivers blocked the Masnaa / Jdaidet Yabous crossing in protest on 10 February 2026, sought an exemption.

As of the date of this briefing, negotiations between Syrian and Jordanian authorities were ongoing regarding phased implementation and infrastructure improvements to the customs yards. The measure, if maintained in its current form, risks diverting Jordan-origin cargo toward the Port of Latakia as an alternative entry route, altering established trade flows across the region.

Outlook & Implications

Syria’s border crossing data from December 2024 through early 2026 presents a picture of rapid, unevenly managed recovery. The headline figures — hundreds of thousands of trucks, nearly a thousand ships, millions of travelers, and a fivefold increase in air traffic — testify to the release of long-suppressed trade demand following sanctions removal and the restoration of centralised border governance. The major port concession deals with DP World and CMA CGM represent a generational shift in the management and modernisation trajectory of Syrian maritime infrastructure.

Invest in Transshipment Infrastructure

The February 2026 truck ban has exposed a critical gap: border customs yards lack the loading equipment, staffing, and space to handle back-to-back cargo transfers at commercial volumes. Without targeted infrastructure investment at Nassib, Bab al-Hawa, and the Lebanon crossings, the policy risks becoming a brake on import supply chains rather than a stimulus for the domestic transport sector.

Develop Harmonised Statistical Reporting

The IMF’s November 2025 technical visit confirmed a lack of reliable economic data in Syria. The new General Authority for Border Crossings and Customs should prioritise digital customs interconnection, standardised data collection at all crossing points, and regular public reporting — enabling evidence-based policy and investor confidence.

Leverage Port Concessions for Transit Hub Status

The DP World and CMA CGM agreements position Tartus and Latakia to become credible Eastern Mediterranean transit hubs. Realising this potential requires parallel investment in road and rail connectivity to the Syrian interior, customs digitisation, and bilateral transport agreements with Gulf states that have historically routed cargo via alternative ports.

Prioritise Air Cargo Infrastructure

Civil aviation recovery has been heavily passenger-led. The cargo throughput figures at Damascus — small relative to regional comparators — suggest significant headroom for air freight growth as the business environment improves and more international carriers resume dedicated cargo services. The free zone at Damascus International Airport is an underutilised asset.

Balance Protectionism with Regional Trade Partnerships

The protectionist direction of Syrian trade policy in early 2026 — manifested in the non-Syrian truck ban and reciprocal restrictions from Jordan — risks alienating the regional partners whose trade volumes are essential to Syria’s economic recovery. A phased, consultative approach to freight regulation, combined with fleet modernisation support for Syrian carriers, would better serve both national and regional interests.

Syria’s border data ultimately reflects a country in an accelerated, fragile, and politically complex reconnection with the global economy. The institutional foundations — the General Authority for Border Crossings and Customs, the new port concession regimes, the restored airports — are in place. The challenge ahead is translating commercial momentum into durable, accountable, and transparent governance of Syria’s frontier gateways, in a manner that supports the country’s broader economic recovery while managing the distributional tensions that rapid trade liberalisation invariably generates.